7 7: Introduction to Cost Accounting Methods Business LibreTexts

Activity-based costing is a costing method that is used to allocate overhead costs with a lot more accuracy by identifying the activities that drive the cost. For example, a technology company might want to understand the exact cost of its product lines using ABC. It will then attribute overheads on the use of resources by various activities like product design, marketing, and customer support. This is, therefore, a useful technique for the company for discovering high-cost problem areas and making strategic decisions to reduce costs and enhance profitability.

Life Cycle Accounting

Under this method, a batch cost sheet is prepared for each batch of products and all costs related to the specific batch are recorded. It is a method of costing used to ascertain the cost of making a single unit of customized product. Under this method, a job cost sheet is prepared for each job and all costs related to the specific job are recorded.

Ask a Financial Professional Any Question

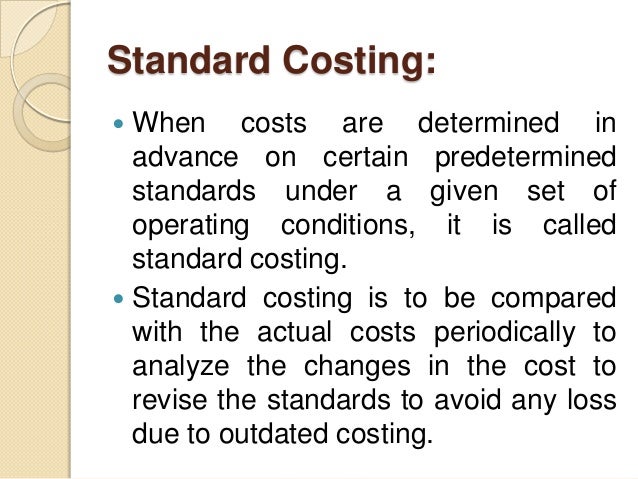

Standard Costing – The preparation and use of standard costs, their comparison with actual costs and the analysis of variance to their causes and points of incidence. This permits the management to investigate the reasons for these variances and take necessary corrective action. For information pertaining to the registration status of 11 Financial, please contact the state securities regulators for those states in which 11 Financial maintains a registration filing.

Which Types of Costs Go Into Cost Accounting?

It is used for big jobs which continue over more than one financial year, e.g., building construction, ship building, dams, civil construction, structural for bridge, etc. The practice of charging all costs, both variable and fixed, to operations, products or processes is termed as absorption costing. Where orders or jobs are arranged in different batches after taking into account the convenience of producing articles, batch costing is employed. The unit of cost is a batch of group of identical products, instead of a single job order or contract. The method is particularly suitable for pharmaceutical industries and general engineering factories which produce component in convenient economic batches.

Cost accounting, however, doesn’t have to abide by these regulations since it’s used internally. In continuous processing, the output of one process becomes the input of the next process and so on until we achieve our finished product. Price your item too high, and you could drive potential customers straight to your competitors. But price the item too low, and your accountant may experience heart palpitations whenever they look at the balance sheet. Deskera ERP is a complete solution that allows you to manage suppliers, track supply chain activity in real time, and streamline a range of other company functions.

This is achieved by analyzing financial data in such a way as to disclose the cost of the units that have been produced. In job costing, the costing of each job undertaken and executed is calculated. This method is adapted in production units that do not involve highly repetitive work. The cost structure is always changing, and as indirect costs increasingly take up a larger slice of the pie.

Activity-Based Costing provides a more accurate picture of product costs which enables better decisions regarding pricing, resource allocation, and process improvement. Additionally, it can help reveal opportunities for cost savings super bowl 2012 a championship in pictures that may not be identified with traditional methods. Explicit cost driver- explicit cost drivers are those which are included in the accounting records of an organization at the time of preparing Financial Statements.

An activity cost driver is Really a measure of frequency and Strength of Demand, set on tasks by cost items. The quantity measure of the resources used/consumed by an activity is called Resource Cost Driver. It is used to assign the cost of a resource to an activity or cost pool.

- Now that you understand the costs involved and how to calculate these let’s take a closer look at the costing methodologies to see the advantages and disadvantages of each method.

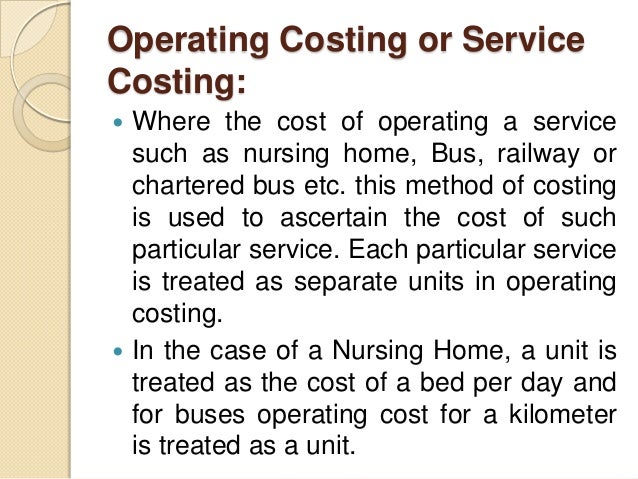

- This is used to determine the costs of services rendered by airways, railways, roadways, hospitals, power houses etc.

- Budgets are prepared, standards are established, actuals are ascertained, and then a comparison is made.

- Katana’s intuitive Insights dashboard provides a clear overview of your sales and manufacturing costs.

- In this method each operation at each stage of production or process is separately identified and costed.

- It is used to assign the cost of a resource to an activity or cost pool.

Estimated costs are definitely future costs and are based on the average of the past actual figures adjusted for anticipated changed in the future. In this method costs are separately collected and accumulated for each process or department. In order to arrive at the cost per unit, the total cost of the process or department is divided by the quantity of production. This method is used in mass production industries manufacturing standardised products in continuous process of manufacturing.